Since the financial crisis, Wells Fargo (NYSE:WFC) performed better than most major banks until recently. Due to the strength of its deposit franchise, its superior cross-selling and its control of costs and risk, the bank demonstrated superior performance and shareholder returns. This was evident in most of the key measures of underlying profitability and in its competitive position in the markets in which it chose to compete and with the clients it chose to serve. Wells Fargo demonstrated more consistent earnings since the financial crisis as a result of its business mix which is less exposed to volatile capital markets and investment banking income. Until recently it did not suffer the same magnitude of legal and/or market-related setbacks as most other major banks. Its management was perceived as being superior. Consequently, Wells Fargo traded at a premium valuation to its peers.

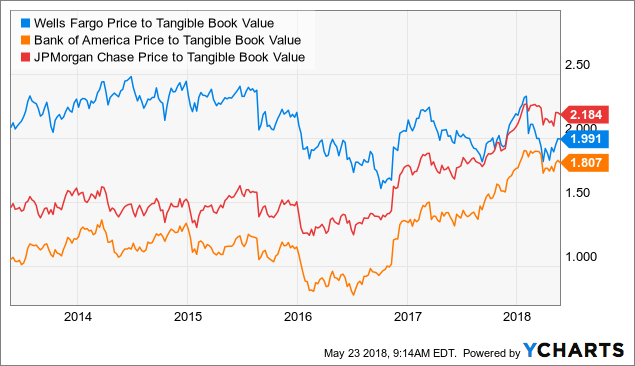

In recent months, as a result of the accounts opening scandal and other sales-related problems, which have been written about in much detail elsewhere, Wells Fargo's relative financial performance has deteriorated and so its premium valuation has unwound. Its stock has significantly underperformed in recent months.

WFC data by YCharts

WFC data by YCharts

WFC Price to Tangible Book Value data by YCharts

WFC Price to Tangible Book Value data by YCharts

Recent Results

The loss of momentum is very evident in Wells Fargo's results. In Q1 2018, its loans and deposits grew by less than the other majors and its total revenues fell 1.4% year on year versus increases of 4% at Bank of America (NYSE:BAC) and 10% at JPMorgan (NYSE:JPM). Net interest and non interest income both fell. Expense performance deteriorated as a result of the substantial increase in compliance and legal costs (US$3.25bn in Q4 17 and a US$800mm litigation accrual in Q1 2018 in connection with the CFPB and OCC consent orders of April 20, 2018). Costs were an area where Wells Fargo used to be best in class. Its revised efficiency ratio as per its 10-Q was 69% in Q1 2018 versus 60% at Bank of America (the big improver) and 56% at JPMorgan (the best in class).

All of this has led to a loss of momentum in Wells Fargo's Pre Provision Profitability ("PPP") and in its Pre-tax Margin. PPP is a metric which prior management often cited as a key measure of its underlying profitability. Wells Fargo's PPP fell 19% in Q1 vs. Q1 2017 in contrast with the significant growth seen at most other major US banks. Its net income in Q1 2018 fell 9% year on year, despite the positive impacts of the Tax Cuts and Jobs Act and a 68% decline in provisions for credit losses as a result of further legal charges. This was in contrast to the improvements seen at most of the other majors (for example net income increased 34% year on year at Bank of America and 35% at JPMorgan). Wells Fargo started from a better position but has underperformed very significantly in recent months. It no longer has a class-leading Return of Assets or Return on Tangible Equity (two key metrics for our valuation framework), and the movement in both of these key metrics has been in the wrong direction in contrast with the others despite a generally favourable operating environment.

Focus on the Trend in Underlying Profitability

The immediate call to make on Wells Fargo is whether its underlying profitability will return to past levels after the various fines are paid, corrective steps are taken and the bank returns to its underlying operating model. Or has Wells Fargo's historically superior underlying profitability been permanently damaged as a result of the recent events, the reputational damage it has suffered and its prior business model being irreversibly changed by the series of restitution measures it has had to take and no doubt will be required to take going forward?

It is very difficult to answer this question at this moment without being an insider and/or without having direct access to the bank's leadership and management. Nevertheless, Wells Fargo has outlined some of its thinking in its recent Investor Day Presentations.

In the Short Term, Expenses are the Key to Improvement

Net interest income is expected to be stable in 2018 as the positive impact of projected higher interest rates is offset by a possible flattening of the yield curve, hedge unwind costs, expected increases in deposit costs and lower earning assets, partly as a result of the asset cap. The bank has sought to reduce its exposure to some higher risk segments (sensible given the stage of the economic cycle), and this may compress loan yields. Tighter credit spreads may also put pressure on commercial loan pricing, although this may reverse given the spread widening of recent weeks. The bank has forecast that the earnings impact of the asset cap is expected to be less than US$100mm, but we still expect that the bank's growth in net interest income will underperform its peers in the short term. Even if rates were to rise, Wells Fargo is less sensitive to this than others. A 100bp upward shock in interest rates is forecast to result in a 3-5% improvement in net interest income in the first 12 months (+US$1.5-2.5bn improvement using 2017 numbers).

So in the short term, expenses are likely to be the key to improvement. The bank has forecast US$4bn of cumulative expense savings by end 2019 excluding legal costs. Specific detailed guidance has been given, and expenses are expected to revert close to 2016 levels by 2019, excluding legals.

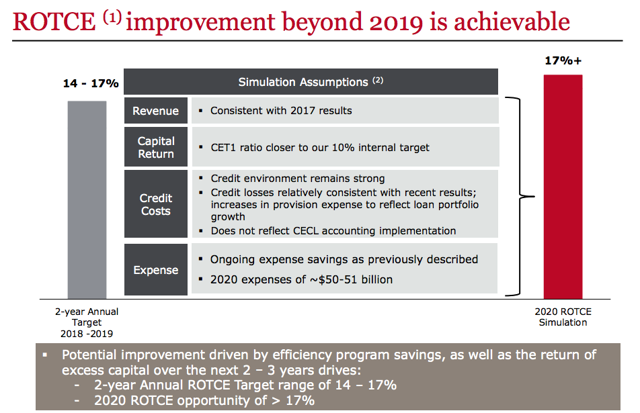

Critically, even though the bank has guided unchanged revenues (conservative given the possibility of higher rates and increased non-interest income), expenses are guided to an aggressive $50-51bn in 2020, resulting in a large improvement in RoTE to 14-17% in 2 years and 17%+ beyond.

Source: Wells Fargo 2018 Investor Day Financial Overview

If this is realised (under the above conservative revenue guidance), using an excess return valuation framework, a stock price of 66.5 is attainable. We believe these assumptions are realistic absent a sustained rise in credit loss provisions and/or revelations of further material legal and/or reputational issues. Provisioning is something that needs watching at this point in the cycle given the very low level of provisions being made at this time.

The longer term and potentially bigger underlying problem that has not been as widely discussed is the lack of revenue growth. Wells Fargo is less exposed to investment banking and so has not benefited from the pickup in revenues that some of its peers saw in 2017 and Q1 2018. However, revenue growth has also lagged in its other businesses, not only versus its direct peers but also against purer play competitors such as U.S. Bancorp (NYSE:USB). All have managed to grow net interest and non-interest revenue in a way that Wells Fargo has not in recent months. This needs further investigation. Wells Fargo is becoming more cautious in business selection at this point in the cycle. Its riskier auto loan, credit card and junior lien mortgage exposure were the main sources of the decline in loans outstanding in Q1. Notwithstanding this, the lack of revenue growth may ultimately constrain valuation once the bank's efficiency ratio returns to its underlying level.

We are long-term holders of the stock since 2009. We would only be buyers of additional stock following material price weakness in the months ahead. This is on valuation grounds and on the basis that Wells Fargo's business model has not been permanently damaged, asset quality will not materially deteriorate in the short term and so its financial performance will return to its underlying trend. However, in the longer term, the lack of revenue growth is a concern and is something we will return to.

Disclosure: I am/we are long WFC, BAC, JPM, USB.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: We invest in bank equity and bank capital securities on a long only basis where we see value.

Carla Mozee

Carla Mozee